Client portal, back-office platform, concept exploration for mobile

Domain

Digital Banking & Treasury Management

~ TLDR ~

Problem

International clients needed a unified platform for treasury workflows (payments, onboarding, compliance), but legacy systems made cross-border transactions and high-risk merchant onboarding prone to compliance and fraud issues.

Approach

Collaborated with product, engineering, and compliance to design scalable workflows across client and back-office apps, emphasizing automated identity verification, bulk transactions, multi-currency support, and AI fraud detection.

My contributions

Directed design strategy across client and back-office applications

Built and scaled the design system for consistent patterns

Designed payment, onboarding, accounting, and compliance workflows

Facilitated workshops with compliance, ops, and engineering

Explored mobile app concepts for future roadmap alignment

Outcomes

Established foundation for unified Core Banking suite

Enabled compliance/risk teams to test and iterate on onboarding + payments

Reduced onboarding friction via shared identity verification

Created scalable design system now used across multiple product lines

Confidentiality: Examples and artifacts are redacted/representative. Flow diagrams omit sensitive implementation details.

Businesses and internal teams were relying on fragmented, legacy systems to manage treasury workflows. Clients needed a single, modern platform to:

Initiate and track a high quantity of ACH, SEPA, and SWIFT transactions (both single and bulk)

Manage cash flow and foreign exchange across multiple accounts and currencies

Verify payees and maintain compliance with KYC/AML regulations

For business clients, this meant reducing friction when moving money domestically and across borders, where regulatory requirements and FX processes often slowed transactions or introduced errors.

For internal risk and compliance teams, the challenge was onboarding high-risk merchants, enforcing anti-fraud checks, and handling complex cross-border compliance rules — all while relying on tools that lacked transparency and scalability.

These gaps created friction for customers, increased compliance overhead, and ultimately limited the company’s ability to scale payment volume across geographies.

Constraints & risk

Designing for a core banking platform meant working within a highly constrained environment where regulatory, technical, and organizational risks all shaped the solution space:

Regulatory complexity: Every flow needed to comply with strict domestic and cross-border regulations (AML, KYC, and FX rules). Missteps could trigger compliance violations, fines, or delays in money movement.

High-risk onboarding: Workflows for underwriting and merchant approvals required balancing user clarity with layered fraud prevention. A design that was too open invited risk; one that was too strict created abandonment.

Legacy adoption: Many business clients were accustomed to manual or siloed systems, so workflows had to feel familiar enough to encourage adoption while still introducing modern efficiencies.

Cross-team alignment: Risk, compliance, engineering, and product stakeholders all had different priorities. Ensuring alignment often meant trading off speed for accuracy, especially in workflows tied to regulatory audits.

Technical constraints: Payment processing logic, third-party integrations (for FX and fraud monitoring), and core banking infrastructure limited how far we could push certain experiences in early releases.

Together, these constraints made it clear the solution had to be incremental, transparent, and defensible — every design decision had to stand up to compliance review while still moving the product forward.

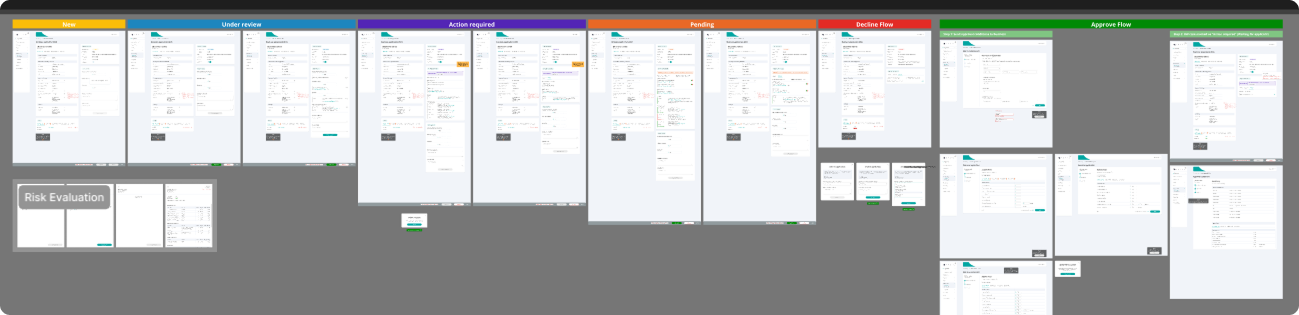

Business application underwriting and risk analysis flows

Approach

To tackle these challenges, I worked closely with product managers, engineers, and compliance SMEs to define a design approach that balanced regulatory rigor, user needs, and long-term scalability. The process blended vision-setting with iterative validation, ensuring each step moved us toward a unified platform:

Shared identity verification layer: Instead of duplicating KYC/AML checks across applications, I designed a single verification flow that served both business clients and internal risk teams. This reduced redundant steps, improved auditability, and gave users a clearer sense of progress.

Bulk transaction workflows: Recognizing that many business clients executed high-volume ACH, SEPA, or SWIFT transfers, I designed a flexible bulk payments module that allowed for importing, reviewing, and executing a high volume of transactions with built-in compliance checkpoints.

AI-assisted fraud monitoring concepts: To support compliance teams, I introduced early prototypes with embedded AI-driven risk evaluation, surfacing anomalies or suspicious patterns within payment and onboarding flows. These concepts helped set direction for how technology could scale human review.

Cross-functional validation: I facilitated workshops with compliance, ops, and engineering stakeholders to stress-test workflows before moving into development. These sessions identified edge cases (e.g., international FX holds, high-value transaction flags) early, avoiding costly rework.

Concept exploration for mobile: While not in scope for initial releases, I sketched mobile onboarding and approval flows. These concepts informed product strategy, ensuring that near-term design patterns could extend seamlessly to future surfaces.

This approach ensured we were not only solving immediate usability challenges but also building the foundation for a scalable, compliant, and future-facing core banking platform.

Key decisions

Throughout the project, I made several design decisions that directly shaped how the platform balanced compliance, usability, and scalability:

Unified identity verification: Early on, we faced the choice of building separate KYC/AML flows for clients, and internal teams, or creating a shared system. I advocated for a unified identity layer that could serve both. This reduced redundancy, made audits easier, and gave clients a consistent experience across applications.

Scalable design system investment: Rather than designing one-off screens, I prioritized enhancing our flexible design system for this project from the start. This decision slowed early delivery slightly but ensured consistency across the client portal, back-office tools, and future product lines, accelerating later iterations.

Progressive onboarding for high-risk businesses: Traditional onboarding demanded large amounts of information upfront, leading to drop-offs. I broke the process into smaller, progressive steps with clearer progress indicators. This improved completion rates while still meeting compliance requirements.

Concept-first approach to mobile: The team debated whether to prototype mobile in full fidelity early on. I pushed for lighter-weight concept exploration instead, which allowed us to shape the roadmap without draining engineering resources from the in-progress client and back-office builds.

Risk-informed bulk payment design: For bulk transfers, we had to decide between giving clients speed or enforcing strict compliance checks. I designed a layered workflow that allowed for high-volume entry but added review points where risk thresholds were met, striking a balance between efficiency and control.

These decisions not only shaped the initial platform but also set standards for how the company approaches designing in regulated, risk-sensitive environments.

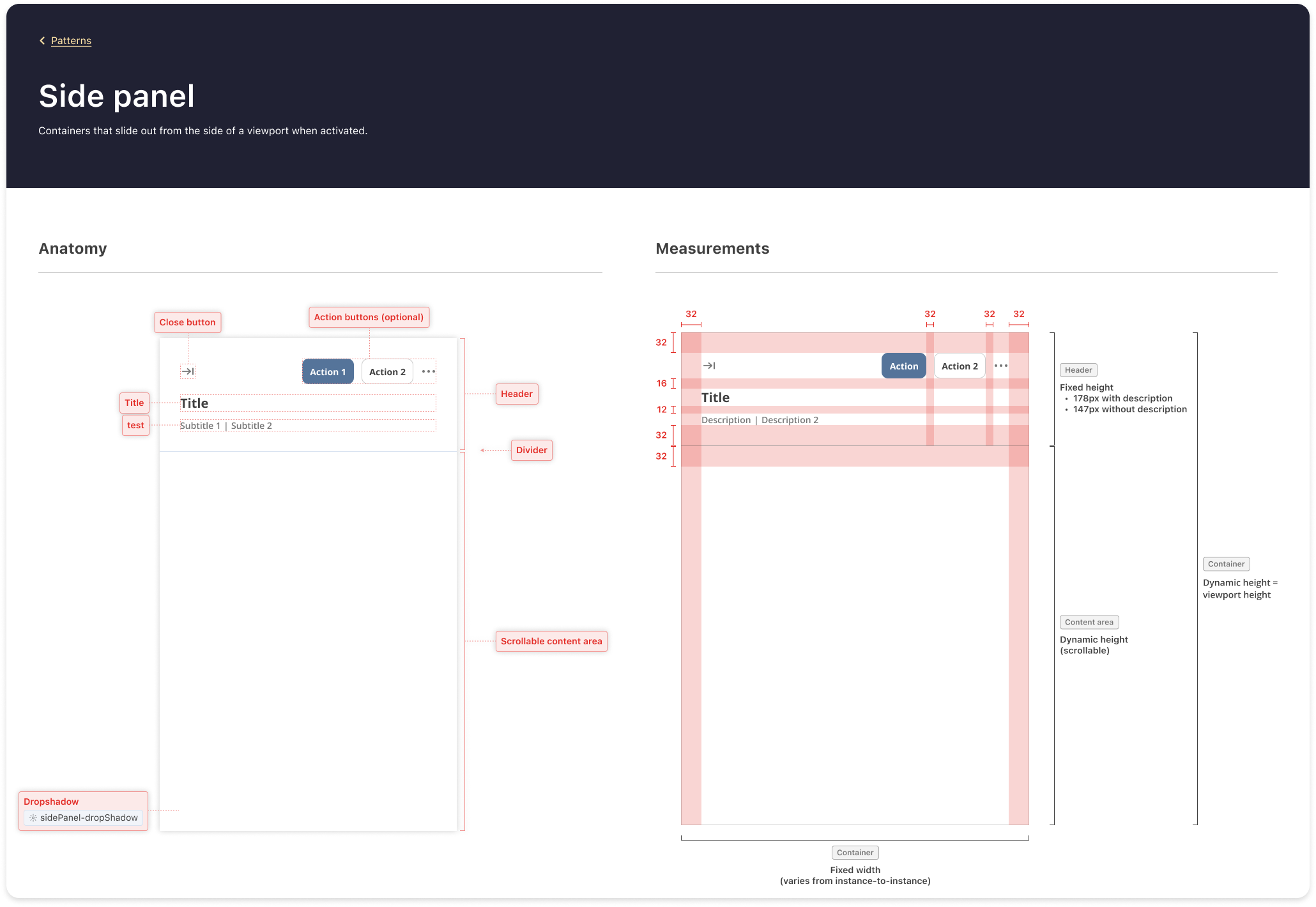

New component specs in the design system

Outcomes & next steps

Although the Core Banking platform is still in development, the design work has laid a strong foundation for current workflows and future expansion:

Unified platform architecture: Established a consistent design framework across client and back-office applications, creating the baseline for scalable treasury operations.

Validated workflows: Payments, onboarding, and compliance flows were designed and tested with cross-functional stakeholders, ensuring regulatory defensibility and usability before build.

Design system adoption: A scalable design system is now in use across multiple product lines, heavily reducing design speed and development debt.

Future enhancements: Concept work has informed upcoming roadmap initiatives, including a client-facing mobile app, card issuing capabilities, and issuing virtual IBANs to support multi-currency treasury management.

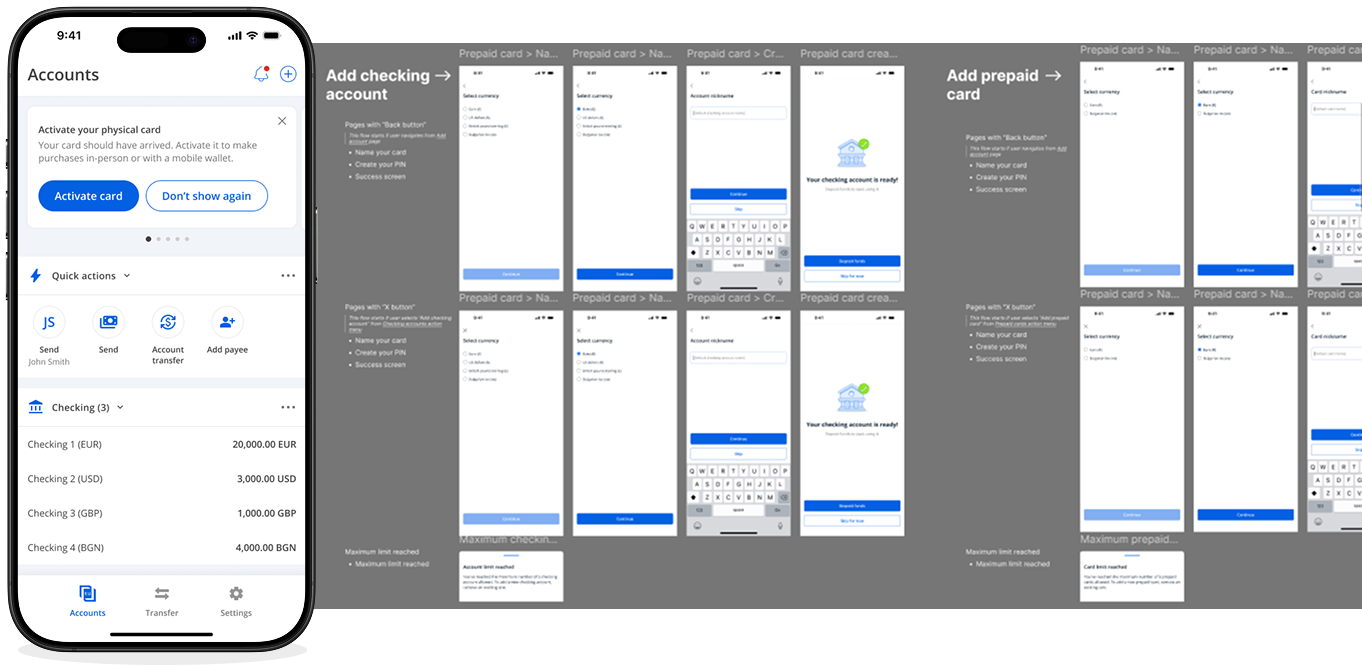

Core Banking mobile app concept and user flow annotations

Next steps: Continue iterative development of the client and back-office platforms, expand AI-assisted fraud monitoring into production, validate mobile concepts with business clients, and extend the design system to cover emerging product areas.

Key takeaway

The Core Banking project showed me the importance of designing with both today’s constraints and tomorrow’s possibilities in mind. By laying a foundation for payments, onboarding, and compliance, I was also shaping a platform that can grow into mobile, card issuing, and virtual IBANs — without redesigning from scratch.

Confidentiality: Examples and artifacts are redacted/representative. Flow diagrams omit sensitive implementation details.

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.